Global Perspective

As was hoped coming into the year, 2018 did see one of the largest IPOs ever, but it wasn’t the name widely touted at the start of the year. With the Saudi Aramco IPO currently on hold, it was instead Softbank Corp which raised $21.3bn becoming the 4th largest IPO on record. This helped push 2018 IPO volume to $209.5bn, up 5% on 2017 despite a 15% drop in deal count. With market volatility and geopolitical concerns it was the first time since 2011 that the number of IPOs in the fourth quarter was less than in the third.

Overall, Global ECM volume fell 17.5% to $720.6bn with a corresponding fall of 15.7% in the number of deals to 5,451 compared to 2017. Naspers sale of a 2% stake in Tencent Holdings for $9.8bn through an ABB was the largest non-IPO of the year and the largest ever ABB completed outside of the United States

Record breaking year for Hong Kong IPOs

The Hong Kong Stock Exchange underwent various reforms in its listing regulations in April, including giving the green light for pre-profit biotechnology company to list and allowing the use of weighed voting rights structures – more commonly referred to as dual-class structures. Under such circumstances, Hong Kong achieved an all-time record high in IPO activity, and became the largest IPO market globally for the year ($33.3bn via 195 IPOs), with New York Stock Exchange ($31.6bn via 70 IPOs) following behind.

The telecommunications and technology sectors were the main contributors for the impressive IPO performance in 2018, raising $12.9bn and $7.6bn respectively. There was a record high of 400 companies applying for IPO listing in 2018, a 76.2% increase from 2017 (227 filings), with 142 companies successfully listed and 190 companies bringing their potential listings to 2019.

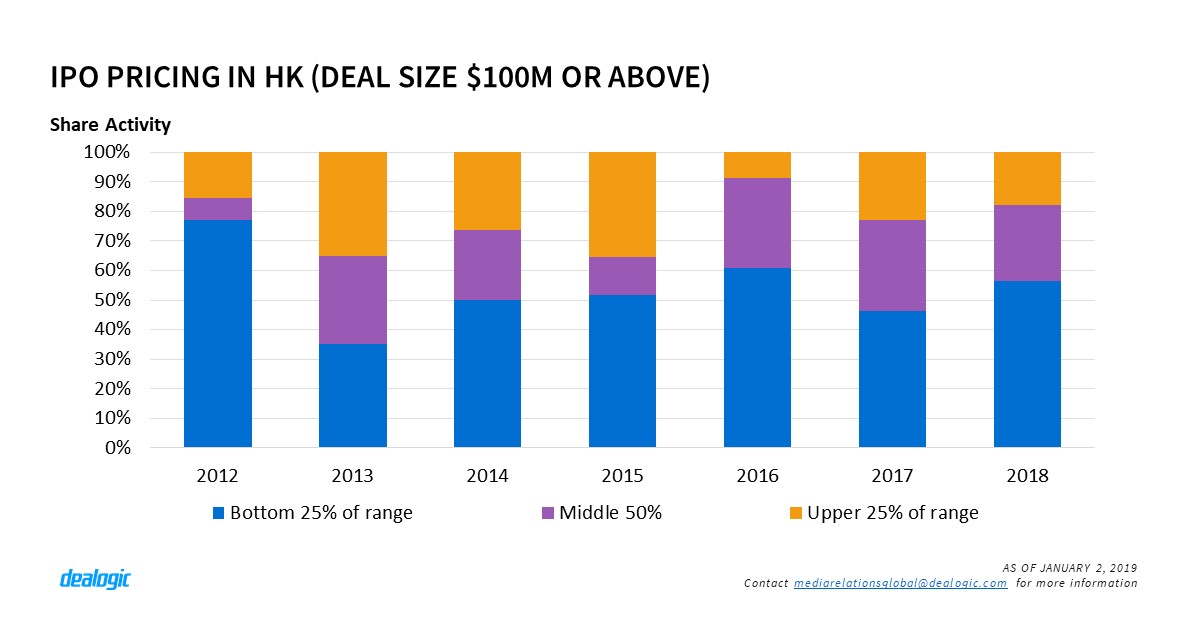

Despite the strong activity in applications for IPO listings, the pricing and aftermarket performance of the companies offered a different story. 56.4% of IPOs priced in the bottom quarter of the marketing range, 25.6% in the middle and 17.9% in the top quarter of the range2. Compared with 2017, there was a 10.3% increase in pricing at the lower end.

With regard to the aftermarket performance of companies on the mainboard, 36.1% traded below the offer price on the first day, compared with 28.6% in 2017. Amongst the 7 companies accepted to list due to the recent regulatory changes, Innovent Biologics performed the best by trading at 72.4% above its offer price as of December 31. 4 others of the 7 were trading below the offer price at the end of the year.

China ECM in deep water – from onshore to offshore

There was a drastic drop of 76.6% in the number of Chinese A-share IPOs in 2018 compared to 2017 as a response to various regulatory revisions by the CSRC that have led to a stricter approval process. Private placements also suffered from the rule change and decreased by 57.0% in 2018. In total, Chinese onshore ECM volume changed from $140.7bn via 745 deals in 2017 to $67.3bn via 309 deals in 2018.

With such a downturn in the domestic market, 122 Chinese companies chose to list overseas, marking the highest offshore listing level since 2010 (145 listings). As expected, Hong Kong (83 deals) and the US (35 deals) continued to be the top two most popular listing locations for Chinese companies.

China also launched the London-Shanghai Stock Connect Scheme and D-share listings in Frankfurt to attract international investment. Qingdao Haier successfully completed the $327m D-share offering on the Frankfurt Stock Exchange in October, while Huatai Securities Co Ltd is expected to raise approximately $500m in a London GDR offering some time this year.

SoftBank IPO setting records

The SoftBank Corp IPO was priced on 10 December 2018 raising $21.3bn, making it the largest ECM deal globally in 2018 and the largest Japanese ECM deal on record. At this level the SoftBank IPO is ranked as the 4th largest IPO on record globally, joining 4 other Asian companies to make it an all Asian top 5 for largest global IPOs on record. Driven by SoftBank Corp’s mega IPO, domestic Japan IPO volume has set a record high of $26.7bn via 97 deals in 2018, breaking the previous record in 1998 ($20.6bn via 86 deals).

EMEA ECM Volume faces a rough 6 year-low

EMEA ECM volume in 2018 totalled $159.6bn, a 39% decline from 2017 and a 6 year-low since 2012 ($144.5bn). 1,347 ECM offerings were brought to market in 2018, a 21% decrease from last year (1,708 deals), which was the largest year for EMEA ECM activity since 2007 (1,930 deals). Worries over interest rates, trade wars, global political uncertainty, Brexit’s deadlock and high volatility levels, led to muted European issuance and weak EMEA emerging markets. This was a reflection of the wider market with the MSCI Europe Index and MSCI EM EMEA Index closing at 1,480.6 and 239.6 on Friday December 28, 2018 respectively, down 18% and 19% for the year from Friday December 29, 2017 (1,796.65 and 296.08).

Germany & Carve-outs: A well-suited couple for EMEA IPOs

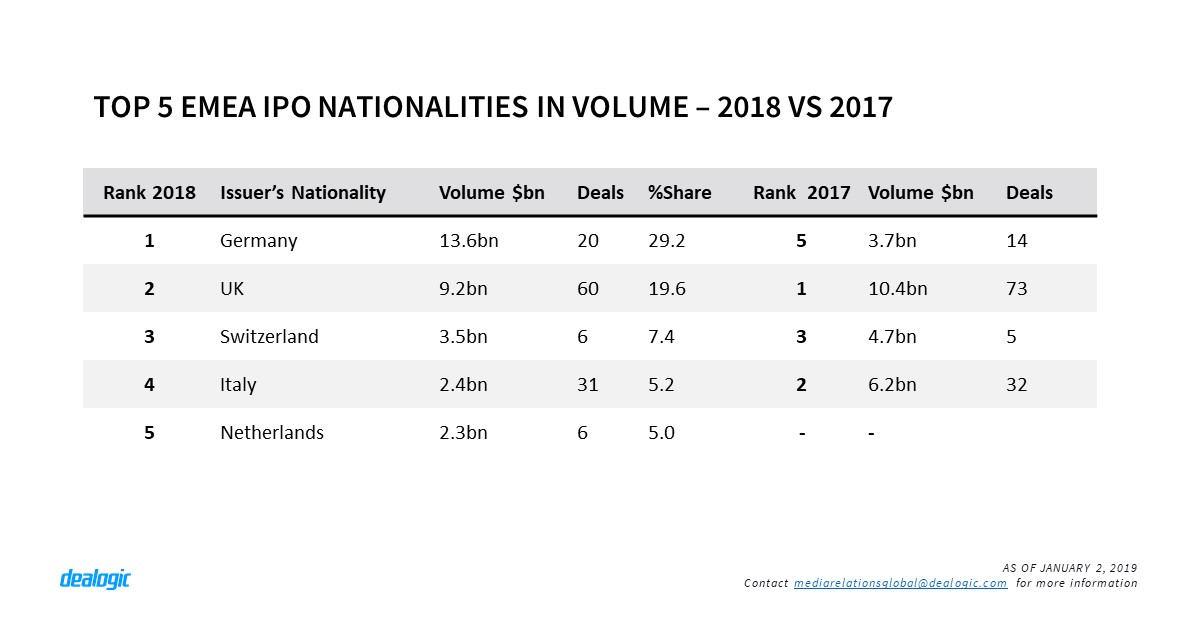

Affected by the above factors, 2018 was a volatile year for the EMEA IPO market that saw a 15% decrease in proceeds to $46.8bn and a 21% decrease in activity to 283 IPOs from 2017 ($55.0bn via 357 IPOs). With most of the top EMEA ECM countries witnessing a decline in their IPO proceeds compared to last year, it was only Germany that saw an increase in IPO volume ($13.6bn) compared to 2017 ($3.7bn). Having priced the fourth and fifth largest IPOs globally, Siemens Heathineers AG ($5.2bn) and Knorr-Bremse AG ($4.4bn), and three of the top five largest EMEA IPOs in 2018, Germany returned in the top of the EMEA IPO rankings in proceeds after 18 years, while it ranked fourth on global 2018 IPO volume, following China, US and Japan.

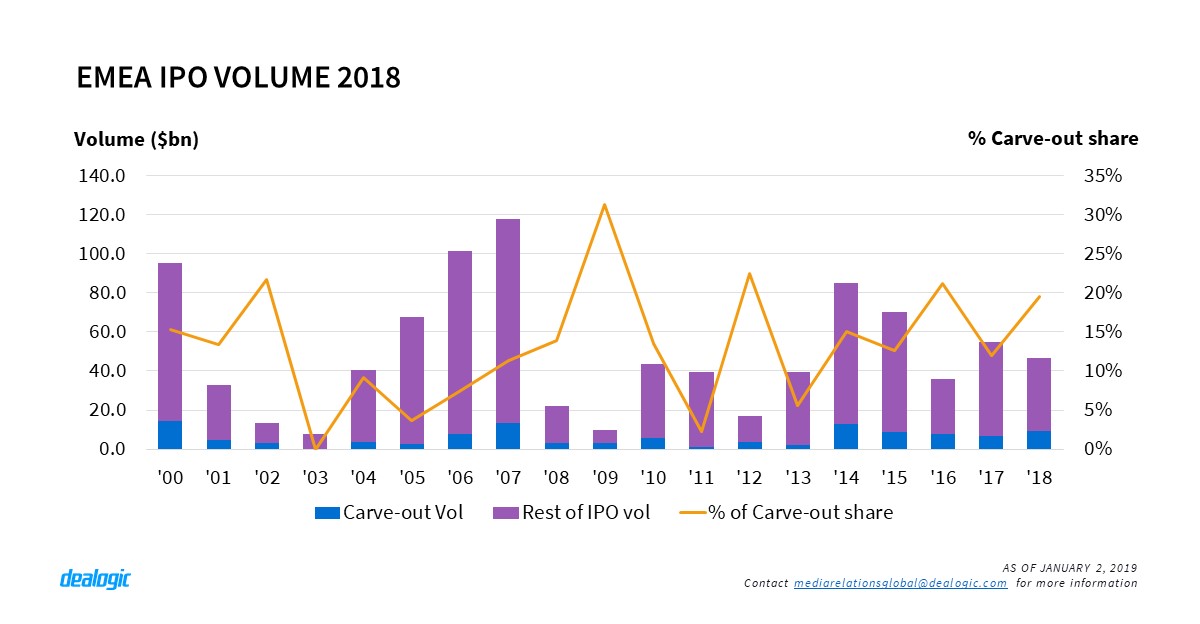

Germany also followed Japan with the second highest volume of carve-out divestments in 2018 ($6.8bn), boosted by two transactions: the carve-out of Siemens Healthineers from Siemens which at $5.2bn was the largest EMEA IPO and second largest Carve-out globally in 2018; and Deutsche Bank’s IPO of DWS Group for $1.6bn.

EMEA carve-out IPO proceeds stood at $9.1bn via 10 transactions in 2018, the largest volume since 2014 ($12.7bn via 15 transactions). Driven by the ongoing macro-economic challenges and the need to focus on core business operations, EMEA carve-out divestments, accounted for 20% of the total EMEA IPO proceeds in 2018 – up 8 percentage points from 2017- the highest percentage since 2016 in volume (21%).

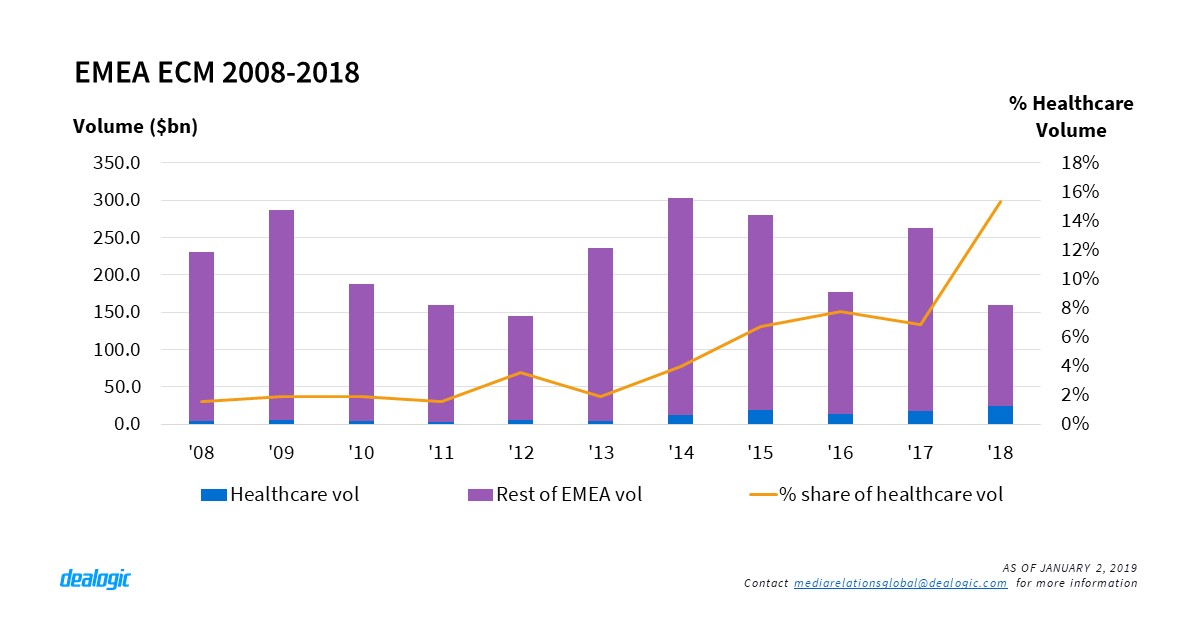

Healthcare is back again after 26 years with EMEA’s largest ECM deal

Backed by the Bayer $7.0bn rights offering – the largest EMEA ECM deal and fourth largest ECM globally in 2018 – the healthcare sector topped the EMEA ECM volume rankings for the first time since 1992, raising a total of $24.5bn via 215 transactions and accounting for 15% of the total EMEA ECM proceeds, the highest share since 1993 when it also accounted for 15%. Finance came second with $23.6bn and then followed Technology with $18.4bn in third although it led in ECM activity with 241 deals.

Another prosperous year for US-listed ECM

SPAC IPOs continued the trend seen last year with 2018 recording the second highest volume on record ($12.7bn via 67 deals) after 2017 ($15.1bn via 74 deals). The size of SPAC IPOs has also been maintained with the average size of SPAC IPOs between 2014-2018 at $172m compared to just $85m in the previous 5 years (2009-2013). 15 of the top 20 largest SPAC IPOs on record have priced in the years between 2016-2018.

The number of banks active in the area has also been on the increase. In the past 5 years new players such as Goldman Sachs ($2.7bn via 13 deals), B Riley FBR ($873m via 5 deals) and Jefferies ($689m via 4 deals) all entered the SPAC field. And already active banks such as Cantor Fitzgerald have also increased their SPAC issuance dramatically over the past 5 years. In 2014, Cantor received credit for SPAC IPOs of $300m via 4 deals compared to $1.6bn via 8 deals in 2018. This has led to Cantor Fitzgerald being the top bookrunner in the US SPAC ranking for 2018.

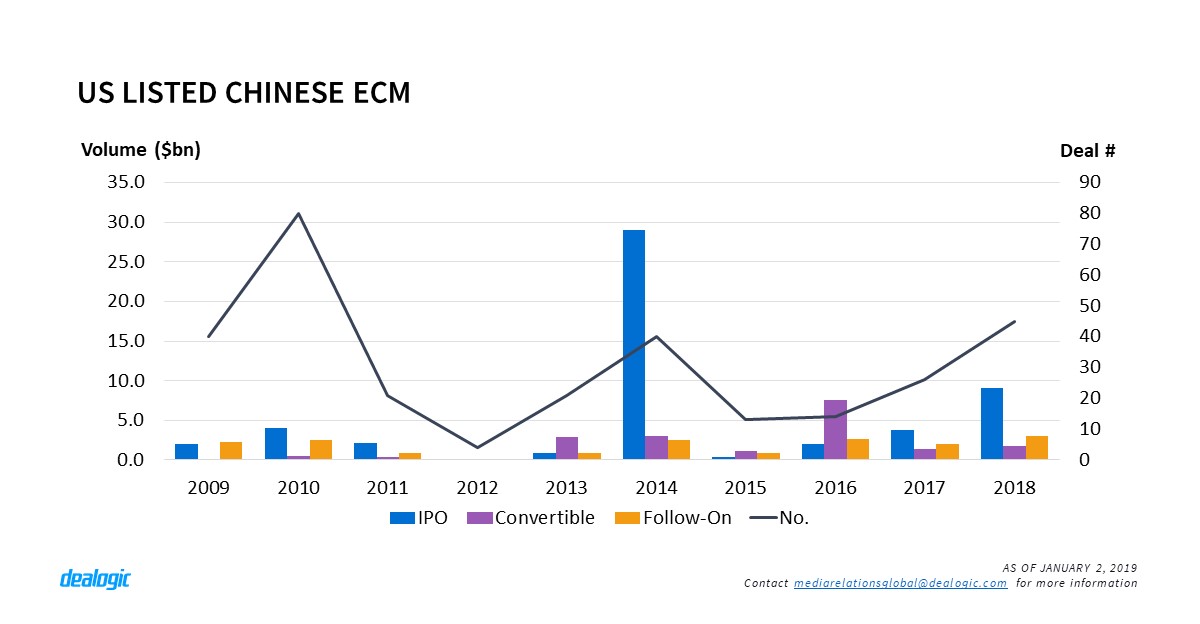

Despite the political tension between the US and China, US-listed ECM for Chinese issuers stood at $14.5bn via 48 deals, the third highest volume on record after $34.7bn via 40 deals in 2014 and $16.7bn via 8 deals in 2000. US-listed Chinese IPOs contributed the majority of the volume with $9.1bn via 31 deals, which is also the third highest US-listed IPO volume on record after 2014 ($29.1bn via 14 deals) and 2000 ($12.4bn via 7 deals).

Tencent Music Entertainment Group, which priced its IPO for $1.1bn on December 11, became the 24th US listed Chinese company to conduct an IPO in the US this year. Against the backdrop of legal action against Tencent Music by an early investor, Tencent Music still raised $1.1bn, which is the 4th largest US-listed Chinese IPO this year. Chinese issuers accounted for the largest share of non-US issuers conduction IPOs in the US, accounting for 64% (30 of the 47) of non-US issuer IPOs.

One bright green spot in Canada

Canada ECM hit its lowest point in more than a decade this year as volume dropped to $19.5bn via 434 deals for 2018 – a 38% decrease from 2017 and the lowest volume since 2003. The traditionally strong sectors like Oil & Gas, Mining, and Utility & Energy all experienced low issuance. The Oil & Gas sector stood at $1.3bn via 20 deals in 2018 compared to $5.9bn via 34 deals in 2017. Mining stood at $2.2bn via 101 deals in 2018 compared to $4.7bn via 147 deals in 2017. Utility & Energy Sector stood at $752m via 6 deals in 2018 compared to $8.8bn via 13 deals in 2017.

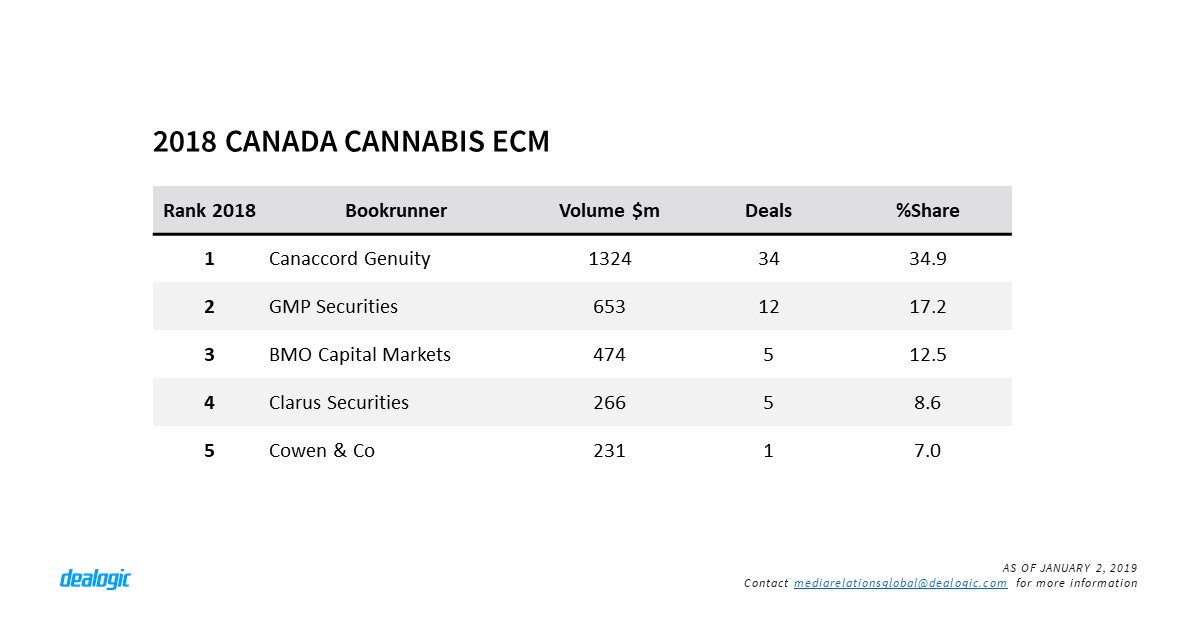

But with the legalization of cannabis in Canada, a new wave of investment continued to rush into the Cannabis industry. In 2018 the Cannabis sector raised $3.8bn via 70 ECM deals compared to just $1.1bn via 44 deals in 2017 – enough to make Cannabis the top industry for ECM volume in Canada in 2018 if treated as a standalone industry. And the size of transactions also increased. Prior to 2018, no Cannabis related business had raised more than $100m through ECM with the largest deal being the $79m offering by MedReleaf Corp in November 2017. Yet in 2018 there were 10 deals above $100m, with Canopy Growth Crop pricing the largest deal in the sector on record with its $461m convertible via Cowen and BMO.

Technology in the Latin American ECM market

While overall Latin American ECM fell 24% to $20.9bn via 67 deals in 2018 compared to 2017 ($27.7bn via 98 deals), the Technology sector saw a boost just like the rest of the world. The Technology sector was the top industry for Latin America with $6.6bn via 9 deals and 2018 was the highest year on record for both volume and deal count. The $2.6bn IPO by PagSeguro Digital was the first $2bn+ IPO priced in the Latin American Technology sector and was the largest IPO from a Latin American company since fellow Brazilian issuer BB Seguridade Participacoes completed its IPO in 2013 ($5.7bn).

– Written by Dealogic ECM Research

Data source: Dealogic, as of January 2, 2019

Contact us for the underlying data, or learn more about the powerful Dealogic platform.